CAGR Insights is a weekly newsletter full of insights from around the world of web.

| Index | 3-Nov-23 | 27-Oct-23 | Change |

| Nifty 50 | 19,226 | 19,060 | 0.87% |

| Nifty 500 | 16,996 | 16,774 | 1.33% |

| Nifty Midcap 50 | 11,306 | 11,044 | 2.36% |

| Nifty Smallcap 100 | 12,962 | 12,641 | 2.54% |

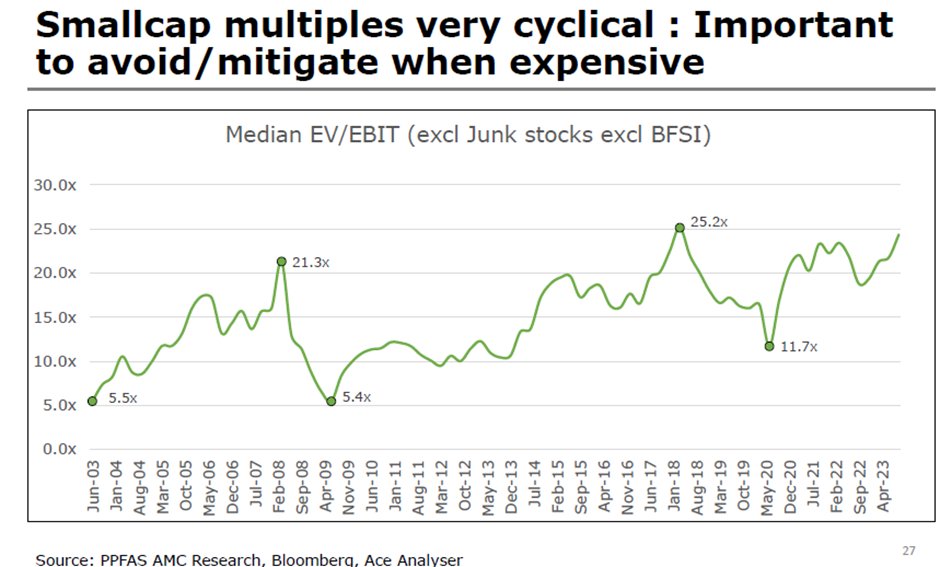

Chart Ki Baat

Monthly Market update

Indian equities dropped in October. Markets have finally corrected after a raging bull market.

But if you see last year’s regression analysis, we are still in a bigger uptrend. The fall has resulted in us being just one standard deviation away from the mean in the larger uptrend in both Nifty and Nifty Midcap indices. The recent conflict between Israel and Hamas in the Middle East is also spooking markets, as analysts worry that US, Iran and other countries will get pulled into the conflict.

Central banks around the world have continued with their hawkish stance, and have suggested holding interest rates higher for a longer period. The Indian indices started falling in the last month as foreign investors began a sell-off in Indian equities.

We are in the amidst of earnings season and as anticipated, large-cap IT services companies posted a muted Q2FY24. FMCG companies’ margins was boosted due to lower raw material prices, but the lag in rural demand is still impacting volume growth. Financial heavyweights delivered robust numbers with a stable asset quality trend. Overall, the earnings season so far has been in line with market expectation.

Here’s the list of curated readings for you this week:

Personal Finance

- Why do we sell winning stocks too early? – Behavioural economists reveal a certain set of biases that affect the human rationality while selling/buying stocks. Read here

- Important things to know about Arbitrage funds – Arbitrage funds have become more popular after the tax benefit of debt mutual funds was taken away. Read here

- Key trends from Q2 earnings of banks – While most of the banks have seen a steady recovery in loan growth and a rise in profits, there is still pressure on the net interest margin due to the interest rates. Read here

- How similar is Investing to gambling? – The article offers insights into how following a systematic approach sets apart the novice investor from the professional stock pickers over the long run. Read here.

- Interview with Charlie Munger – The first ever podcast episode wherein Charlie Munger offers advice and lessons for the investors and reflects on his partnership with Warren Buffet at Berkshire Hathaway. Read here

Economy

- Increase advertising spends of top FMCG players – The market share of listed players has declined due to re-entry ofregional brands into the market pertaining to low raw material costs. This intensifying competition has brought on a new challenge for FMCG players – increased advertising spends. Read here.

- The Amazon Vs Flipkart battle – While there has not been a clear winner in this battle yet. One of the main themes this holiday season, is consumers’ willingness to spend more on luxury goods—a trend that has spread widely and isn’t limited to any one niche. Read here.

- Outlook Start-Up performers 2023 – Indian start-up ecosystem ranked from best to worst with respect to the city clusters, the Delhi-NCR cluster tops the list. Read here

- Outsourcing 2.0: The Global Capability Centre Boom in India – Due to the west grappling with massive labour shortages, there has been an instrumental increase in the Global Capacity Centres (GCC) set up in India. Read here

****

Check out CAGRwealth smallcase portfolios here.

****

That’s it from our side. Have a great weekend ahead!

If you have any feedback that you would like to share, simply reply to this email.

The content of this newsletter is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction. The content is distributed for informational purposes only and should not be construed as investment advice or a recommendation to sell or buy any security or other investment or undertake any investment strategy. There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information outlined in this newsletter unless mentioned explicitly. The writer may have positions in and may, from time to time, make purchases or sales of the securities or other investments discussed or evaluated in this newsletter.