Being a new parent is a special experience and comes with a learning curve that knocks the sleep off many, quite literally. Surviving on three hours sleep routine is no joke. So is ensuring your finances are as tough as your baby’s grip on your finger. After all, you have an additional life depending on you for survival. Yet, in the midst of the whirlwind a new baby gets into our routines, many give our financial health a slip. Some of these missteps could be costly in the future.

Here are top 5 financial mistakes new parents make and how to avoid them.

Mistake #1: Failing To Make A “Baby Budget”

Having a baby is an experience that’s hard to be taught. The baby brings surprising changes to our lives. But one predictable change is extra expense. Regular doctor check-ups, supply of diapers, formula and other common baby items are not surprises and yet, most new parents fail to allocate a certain amount in their budget for the baby expenses. Every new parent need to carve out a place for the baby in the budget before the baby arrives. Experts advice to start living out that way couple of months before the baby arrives to get used to the change in your

expenses.

So, if you are an expecting parent, put some thought into the potential expenses and make a “baby budget”. If you already have the bundle of joy with you, it’s not too late to plan one now. And do not forget to add emergency funds to your budget plan too!

Mistake #2: Overspending

A direct impact of not having a baby budget is overspending and boy, is it easy to overspend on your new baby! The baby may be tiny but the expenses are enormous. The price tags attached to the shiny new stroller, or the whole stack of new clothes (which she is going to outgrow in a few weeks) could be a real eye opener! But resisting the cute, little baby stuff is hard. New parents spend on too many toys, too many clothes, too many “extra” bottles, bibs, pacifiers

because “just in case”. There is no end to it. At the end of the month, you struggle to figure out why you have no money to buy a shirt because well, you didn’t use the extra-soft burp cloth when the baby happily puked on you. Don’t make this mistake.

Babies are easy to please. They don’t need too much of anything but your attention. Stick to your baby budget and buy only the absolute necessities like new bottles. Don’t hesitate to ask for used toys, clothes from other members of the family or friends with older children. There is no shame in it. You are not only being smart about how to manage your finances, you are also inculcating a healthy money habit in your family. This will ultimately be adopted by your

fast-growing child.

Mistake #3: Life Insurance

A baby’s arrival is special but it’s a life long responsibility that spans from her basic needs of food and shelter through health, education and marriage. The costs add up quickly. According to a 2011 report by The Economic Times , the average cost to raise a child is INR 54.75 Lakhs. If the primary breadwinner dies, what happens to your child’s future? It’s an uncomfortable thought but it’s a responsibility that the new parent needs to take with utmost sincerity. And yet, many new parents make the mistake of not reviewing their life insurance after the birth of their

child. This may be unintentional or ignorance.

Fortunately, it’s not rocket science to fix this mistake. The first step is to estimate the expenses of your family including house, health, child’s education, wedding. As a general rule of thumb, it’s recommended that your life insurance be at least five times your annual salary and the other

expenses mentioned above. If you don’t have a life insurance yet, get one today. And make sure your new baby is added as a beneficiary along with your spouse.

Mistake #4: Child Education Savings

The cost of higher education is rising by a whopping 20% yearly. That means what costs INR 20 Lakhs today will cost an incredible INR 95 Lakhs by 2025. What it means to you is saving for your child’s education is an immediate need. But in the midst of paying for diapers and overspending on toys, new parents let this important savings slip by until a few years. Even waiting till the child turns four years old is a big loss in the long term.

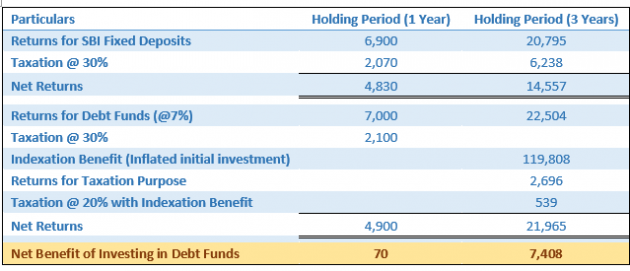

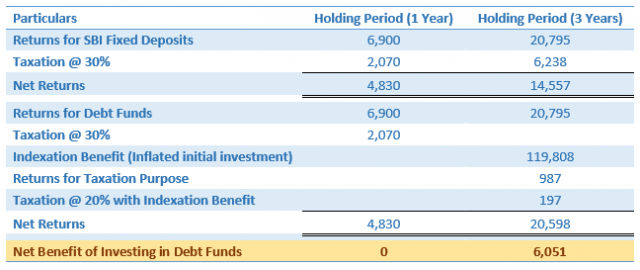

Saving for your child’s education should begin from the day your baby arrives. Investing in mutual funds through SIPs is one of the most effective ways to grow and protect your investments in long term. Companies like CAGRfunds have proven how easy and quick it is to get started with goal-specific investments . What more, CAGRfunds also provides tools to track your investments any day and any time.

Mistake #5: Protecting Your Retirement Savings

It is amazing how our priorities drop to somewhere at the bottom of the list once the baby arrives. Rightly so. After all, you are the parent with the humbling responsibility of giving the little guy a nourishing life. Yet, the baby will one day grow into an adult and leave the nest to pursue his own independence. Until then, you have saved and spent a substantial amount of your earnings on making the child able enough to pursue his dreams. So, once he leaves, where does it leave you financially? It’s important to remember that you are growing older with the child. Your earning years are shrinking. Are you going to forego your retirement savings to pay for your child’s growing expenses?

This is a tough situation but we are a big proponent of protecting your retirement savings with both hands (and legs, if possible!). Your ability to earn more diminishes as you grow older. In fact, your salary pretty much flattens once you hit 40. Which means your best earning years are the first 20 years of your career and that’s exactly when you can save the most. It is imperative that your retirement nest is secured with regular saving and investment plans and is

untouchable through the years of child-rearing.

A new-born baby is the center of joy and pride for parents and nothing in the world matches the happiness. This event could be daunting too but it could be made easier with proper financial planning. Be smart and avoid these financial mistakes new parents make. Your child will thank you for it!