CAGR Insights is a weekly newsletter full of insights from around the world of the web.

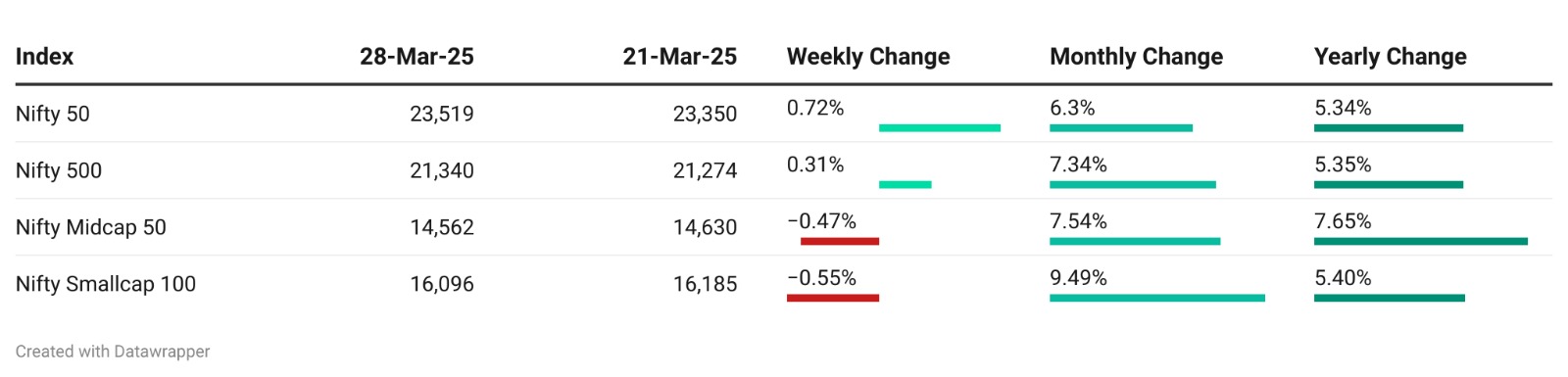

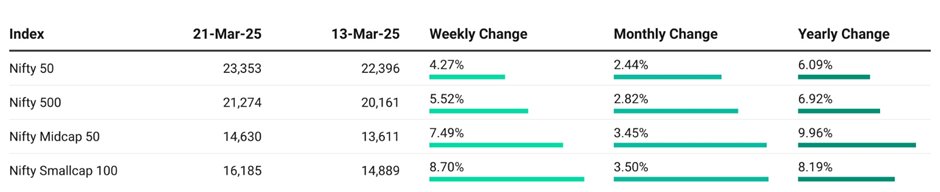

Chart Ki Baat

Tariffs Imposed By US

Gyaan Ki Baat

Investing Wisdom from Buffett’s 1989 Letter

Warren Buffett’s 1989 letter to Berkshire Hathaway shareholders is a masterclass in avoiding pitfalls and embracing timeless investing principles. It’s not just about celebrating success—it’s about dissecting mistakes and learning from them. Here are the standout lessons from this brutally honest reflection:

1. The Power of Tax Deferral: Let Compounding Work for You

Buffett highlights how frequent selling erodes the magic of compounding through taxes. His thought experiment is eye-opening: deferring taxes can turn Rs 1 into Rs 9.2 lakh over 20 years, compared to Rs 2.9 lakh if gains are taxed along the way. The lesson? Avoid unnecessary selling and let your investments grow undisturbed.

2. Look-Through Earnings: Seeing Beyond the Surface

Reported earnings often miss the full picture. Buffett emphasizes “look-through earnings,” which include profits reinvested by investee companies that don’t show up on income statements. Trusting skilled managers to reinvest retained earnings can yield better results than demanding dividends—a reminder to focus on long-term value creation.

3. Beware the EBITDA Illusion

Buffett critiques Wall Street’s obsession with EBITDA during the leveraged buyout craze of the 1980s. Ignoring depreciation and capital outlays is like pretending a broken engine doesn’t matter because the car still rolls downhill. Real businesses need maintenance, and debt-fueled acquisitions often lead to financial instability. Always evaluate cash flows realistically.

4. Time Is the Friend of Quality Businesses

Buffett’s reflection on his “cigar butt” investing mistakes reveals a profound truth: mediocre businesses erode value over time, while great businesses compound it. Instead of chasing bargains, focus on quality companies with enduring competitive advantages—ones that can reinvest capital at high returns.

5. Avoid Tough Problems, Focus on Easy Wins

Buffett learned that solving complex business problems isn’t worth the effort. Instead, he advocates tackling simple opportunities—a philosophy that aligns with his preference for businesses with straightforward economics.

6. Partner with Great People

Buffett underscores the importance of associating with trustworthy and capable managers. Mediocre management in poor businesses won’t guarantee success, but great partners in good businesses can achieve wonders.

Takeaway for Investors Today

Buffett’s lessons resonate deeply in today’s financial landscape, where inflation, market volatility, and speculative bubbles dominate headlines. His advice is clear: prioritize quality over quantity, trust compounding, avoid shortcuts like EBITDA illusions, and partner wisely. Above all, remember that avoiding mistakes is often more valuable than fixing them later—a principle that applies not just to investing but to life itself!

Personal Finance

- EPFO removes two more claim settlement requirements: EPFO has simplified the claim settlement process by removing the requirement to upload cheque images and attested bank passbooks for online claims. It also eliminated the need for employer approval to seed bank account details with UAN. These changes will benefit millions, reduce claim rejections, and streamline procedures.Read here

- Guide to all financial changes from April 2025: Credit cards, income tax, mutual funds and more: As the new financial year 2025-26 starts today, multiple regulatory changes will take effect across mutual funds, credit cards, UPI transactions, taxation, and GST. To know more about the changes. Read here

- Here’s how NRIs can benefit from buying health, term insurance in India: Non-Resident Indians (NRIs) can access affordable health and term insurance in India, benefiting from an 18% GST refund when premiums are paid from NRE accounts. Additionally, NRIs can claim tax deductions under sections 80C and 80D. Term insurance offers tax-free death benefits, ensuring financial security for families. Read here

Investing

- Understanding the psychology of investing matters more than ever: In times of market volatility, investors should maintain a long-term perspective, avoiding emotional decisions driven by short-term fluctuations. Emphasizing discipline, decision journaling, and understanding risk can help investors stay focused and weather market downturns for future gains.Read here

- Would $2M at 23 Make You “Set for Life”? Is $2M at 23 enough to be “set for life”? It depends! While it offers incredible freedom, it might not last forever without smart investing, frugality, or extra income—especially as inflation creeps in. Find out if you could really live off it! Read here

- What investors should learn from the correction in small-cap stocks? From 2020 to 2024, investors bet on small-cap stocks, assuming high risk guaranteed high returns, with the BSE SmallCap Index rising 571%. However, a recent 18.5% drop shows that higher risk doesn’t always lead to higher returns, challenging this belief. Read here

Economy & Sector

- Trump’s Tariffs & India’s Economy | How Will India Navigate the Economic Challenges? Donald Trump imposed a 27% import duty in India, citing unfair trade practices, while claiming India charges a 52% tariff. India’s Commerce Ministry is assessing the impact and exploring new trade opportunities, as US-India trade discussions continue for a Bilateral Agreement. Read here

- India’s growth to be highest among advanced, emerging G20 nations: Moody’s: Moody’s forecasts India’s GDP growth at 6.5% for FY26, the highest among G-20 nations, driven by tax reforms and monetary easing. Despite global risks, India’s large, domestically driven economy, low external vulnerability, and strong capital markets ensure resilience.Read here

- RBI governor says next decade will be crucial in shaping financial architecture of Indian economy: RBI Governor Sanjay Malhotra emphasized the bank’s evolving role in balancing price stability, financial stability, economic growth, and technological advancements. He committed to expanding financial inclusion, improving customer services, and strengthening the financial system while upholding core values of integrity and transparency. Read here

****

Check out CAGRwealth smallcase portfolios

Our smallcase portfolios are ranking well in the smallcase universe in terms of 1-year returns.

• CFF (launched in June 2022) – Ranked 1st amongst smallcase with medium volatility.

• CVM (launched in May 2022) – Ranked among Top 20 across the Momentum smallcase universe.

Do check it out here

****

That’s it from our side. Have a great weekend ahead!

If you have any feedback that you would like to share, simply reply to this email.

The content of this newsletter is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction. The content is distributed for informational purposes only and should not be construed as investment advice or a recommendation to sell or buy any security or other investment or undertake any investment strategy. There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any information outlined in this newsletter unless mentioned explicitly. The writer may have positions in and may, from time to time, make purchases or sales of the securities or other investments discussed or evaluated in this newsletter.