The other day, my mother asked me to teach her cycling. I went speechless for a few minutes, until she spoke up – “I taught you cycling when you were three. Why can you not spend time teaching me now?” I wish I could tell her, “Mom, I was three and you are Sixty – Two!!” But nonetheless, we took an attempt. And what happened next – Umm, another story, another day!

But thank to almighty, she did not come up with a similar argument for money. Imagine my situation had she said “I started building your college fund even before you were born. Why can you not give me an equally hefty amount to retire peacefully?” Phew!

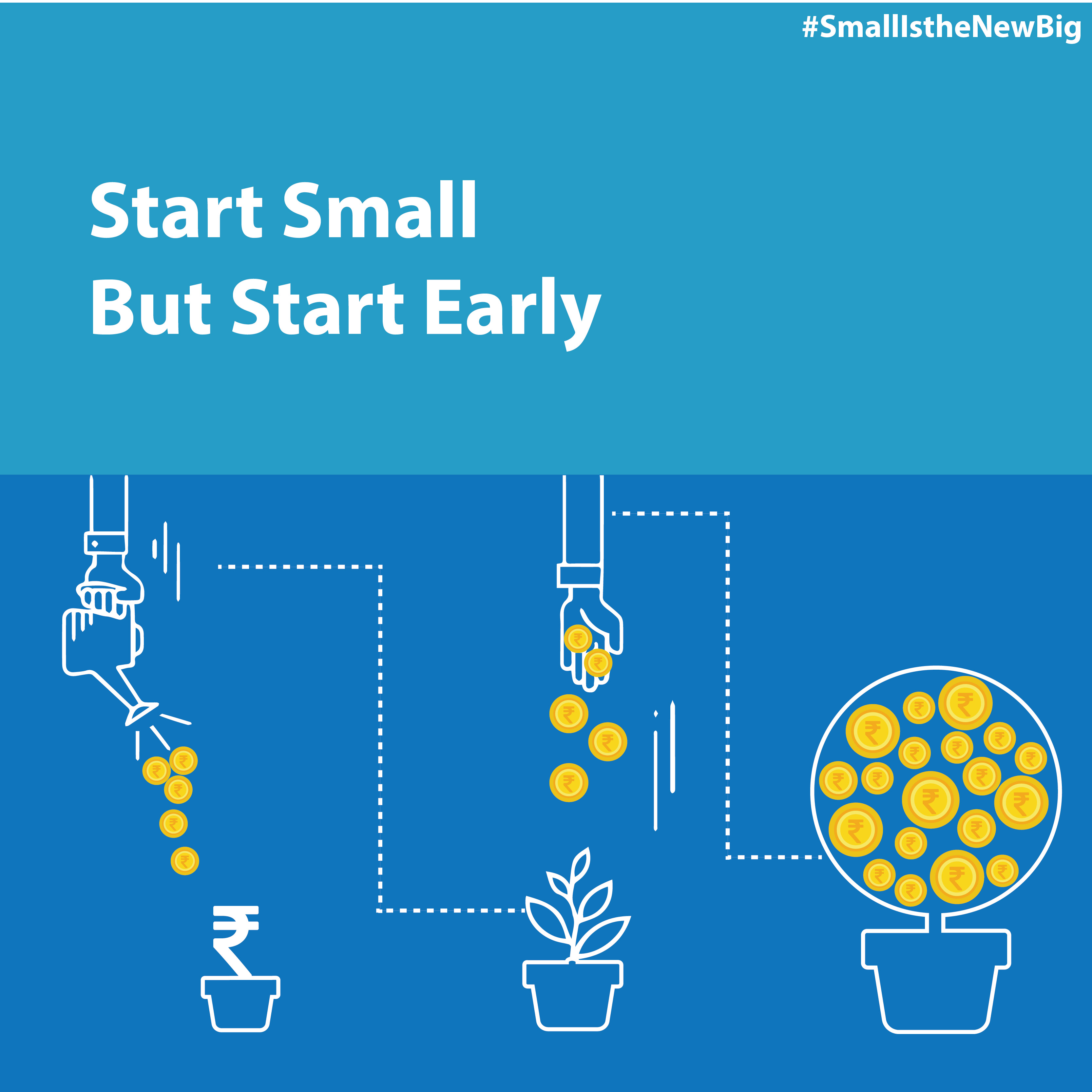

Not sure if I can give her a large enough fund for her retirement, but I surely don’t want to be saying that to my kids. Certainly, there are some things which are better started early in life!

I could not be more convinced when I did some math to understand the benefits of starting to invest early. Assume that today is your 25th birthday and you start investing Rs. 5,000 every month. I get inspired by your decision and start investing the same amount every month. And hey, Happy Birthday to us! I turn 35 today!

Years continue to pass and we continue to invest Rs. 5,000 every month. At the age of 60 I decide to retire and that is when I feel that it is time I make use of the wealth I have created for so long. So I login to my investment account and whoa… what do I see? At an average annual return of 14%, I created wealth amounting to Rs. 1.3 Cr. Satisfaction redefined.

But 10 years later, when you turned 60, that is when I realized what regret truly feels like. At the same average annual return of 14%, you had created a wealth pool of Rs. 5.6 Cr.!!

Perplexing! How was that even possible? 4 times the amount of wealth I created?

Yes my friend, that is the impact a difference of 10 years can make. While a simple mathematic calculation will present to you this fact, the logic behind this is in the “Power of Compounding”.

“Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it” – Albert Einstein

Wondering how it works? Assume that my investment of Rs. 5000 in the first month grows to Rs. 5,050 by the second month. So, in the second month, I am actually investing Rs. 10,050 (5,050 from previous month and a fresh 5,000 for the current month).

The above example presents some very critical learnings.

In the prime of our youth, we have a tendency to be a little generous as far as our spending habits are concerned. If we avoid reckless expenses and shift a defined amount towards monthly investments, the benefits will be visible once the invested amount matures.

Secondly, early on in life, it is relatively easy to park a part of our salary in good investment instruments every month. Such small investments, when accumulated over time, will give us the financial security we have always needed in our lives.

How do we help?

At CAGRfunds, we help you start investing through SIPs. No matter how small you want to start, we help you create wealth in the long run.

To know more whatsapp us on +91 97693 56440